移除 class_weight='balanced' 參數,讓模型學習數據原本的偏斜狀態。

在 backtest_strategy 中啟用信心閾值。

同時修正一下空頭信號的浪費,一個更穩健的空頭濾網應該是當模型極度不看好多頭,且 RSI 進入超買區域時。

for i in range(1, len(df_test)):

price_now = df_test["close"].iloc[i]

rsi = np.nan_to_num(df_test["RSI"].iloc[i], nan=50)

proba = df_test["Proba"].iloc[i - 1]

atr = np.nan_to_num(df_test["ATR"].iloc[i], nan=0)

# -------------------

# 1️⃣ 進場邏輯

# -------------------

if position is None:

if proba >= confidence_threshold and rsi > rsi_long_entry:

position = "long"

entry_price = price_now

entry_capital = balance * position_size_ratio

entry_units = entry_capital / entry_price

balance -= entry_capital * fee_rate # 手續費

if debug:

print(f"[BUY] @ {price_now:.2f}, Proba={proba:.2f}")

elif (1 - proba) >= confidence_threshold and rsi < rsi_short_entry:

position = "short"

entry_price = price_now

entry_capital = balance * position_size_ratio

entry_units = entry_capital / entry_price

balance -= entry_capital * fee_rate

if debug:

print(f"[SELL] @ {price_now:.2f}, Proba={proba:.2f}")

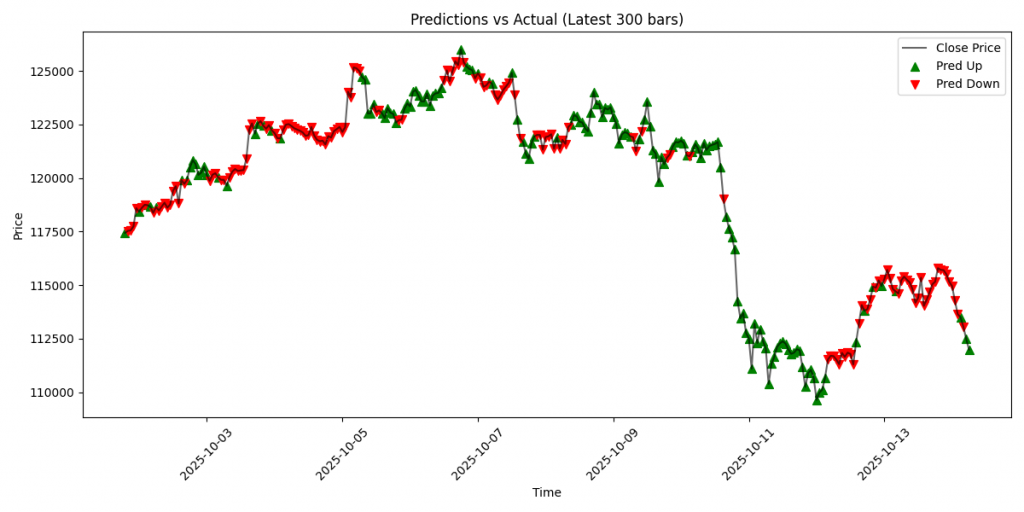

以下是修正後的結果

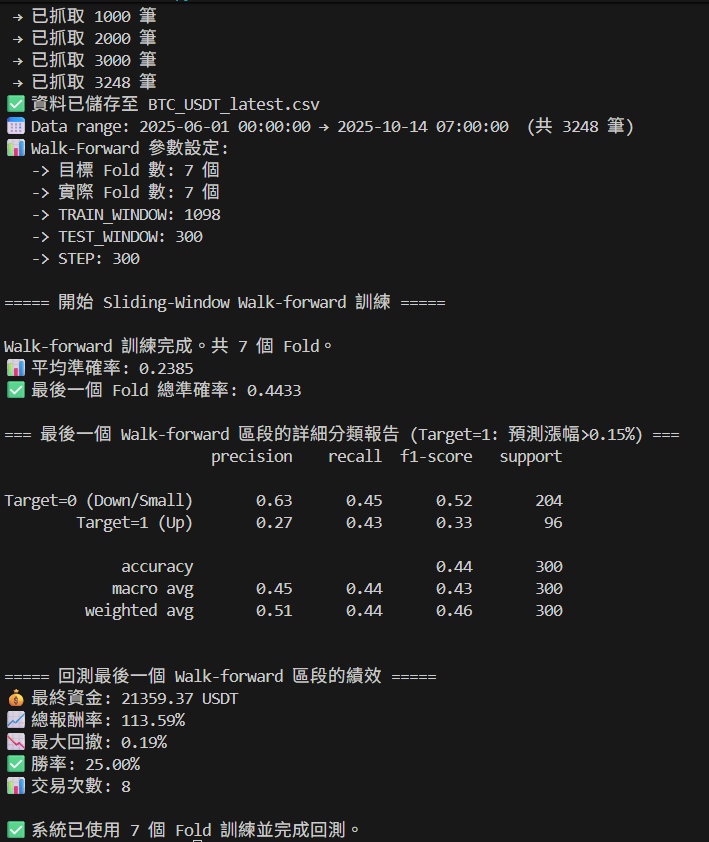

召回率大幅回升! 模型不再極端保守,敢於識別上漲信號了。

但是精確度下降。而這是預期行為,因為模型現在更常猜測,所以猜錯的比例增加。

下一步就是要提升精確度

xian23

xian23