至少要知道交易次數和總獲益點數。

ReportManager.py

class ReportManager:

def __init__(self):

# 交易次數

self.Times = 0

# 總獲益

self.Profit = 0

TradeManager.py

class TradeManager:

def __init__(self, report, strategy, ticks):

self.Tick = None

self.Report = report

self.Strategy = strategy

self.Strategy.OnBuy = self.OnBuy

self.Strategy.OnSell = self.OnSell

self.Ticks = ticks

def OnBuy(self, ds, data):

if self.Tick is None:

tick = self.Ticks.Sequence.pop(0)

print((

f'[BUY]\n'

f'ON PRICE {tick.price} AT {tick.time:%Y-%m-%d %H:%M:%S}\n'

))

self.Tick = tick

def OnSell(self, ds, data):

if self.Tick is not None:

tick = self.Ticks.Sequence.pop(0)

# 遞增交易次數並加入本次獲益至總獲益

profit = tick.price - self.Tick.price

self.Report.Times = self.Report.Times + 1

self.Report.Profit = self.Report.Profit + profit

print((

f'[SELL] PROFIT {profit}\n'

f'ON PRICE {tick.price} AT {tick.time:%Y-%m-%d %H:%M:%S}\n'

))

self.Tick = None

Strategy.py

import abc

import events

class Strategy(abc.ABC, events.Events):

__events__ = ('OnBuy', 'OnSell')

@abc.abstractmethod

def Feed(self, data):

return NotImplemented

Buy3RK1BKAndSell3BK1RK.py

class Buy3RK1BKAndSell3BK1RK(Strategy):

def __init__(self):

self.Bars = []

def Feed(self, data):

status = 0

if data.open > data.close:

status = +1

if data.open < data.close:

status = -1

if sum(self.Bars) == +3 and status == -1:

if self.OnBuy is not None:

self.OnBuy(self, data)

if sum(self.Bars) == -3 and status == +1:

if self.OnSell is not None:

self.OnSell(self, data)

self.Bars.append(status)

if len(self.Bars) > 3:

self.Bars.pop(0)

DataSource.py

import abc

import events

import munch

class DataSource(abc.ABC, events.Events):

__events__ = ('OnData')

def __init__(self, name, option):

self.Name = name

self.Option = munch.munchify(option)

self.Sequence = []

@abc.abstractmethod

def Setup(self):

return NotImplemented

@abc.abstractmethod

def Start(self):

return NotImplemented

MongoDataSource.py

import munch

import pymongo

class MongoDataSource(DataSource):

def Setup(self):

self.Client = pymongo.MongoClient(

f'mongodb://{self.Option.Username}:{self.Option.Password}@{self.Option.Host}:{self.Option.Port}/'

)

self.Database = self.Client[self.Option.Database]

def Start(self):

cursor = self.Database[self.Option.Collection].find().sort([('created', 1)])

for doc in cursor:

doc = munch.munchify(doc)

self.Sequence.append(doc)

if self.OnData is not None:

self.OnData(self, doc)

main.py

from MongoDataSource import *

from TimeSeriesManager import *

from Buy3RK1BKAndSell3BK1RK import *

from TradeManager import *

def main():

def k1min_OnData(ds, data):

data.time = data.time + datetime.timedelta(minutes=1)

k1min = MongoDataSource(

name='TXF-1MINK',

option={

'Username': 'root',

'Password': 'root',

'Host': 'localhost',

'Port': 27017,

'Database': 'backtest',

'Collection': 'k1min'

}

)

k1min.OnData += k1min_OnData

ticks = MongoDataSource(

name='TXF-TICKS',

option={

'Username': 'root',

'Password': 'root',

'Host': 'localhost',

'Port': 27017,

'Database': 'backtest',

'Collection': 'ticks'

}

)

strategy = Buy3RK1BKAndSell3BK1RK()

# 將交易統計管理器、策略與歷史 Tick 資料源傳入交易執行管理器

trade = TradeManager(report, strategy, ticks)

def tsm_OnData(ds, data):

if ds.Name == 'TXF-1MINK':

strategy.Feed(data)

tsm = TimeSeriesManager()

tsm.DataSources.append(k1min)

tsm.DataSources.append(ticks)

tsm.OnData = tsm_OnData

tsm.Setup()

tsm.Start()

# 輸出交易統計結果

print((

f'[REPORT]\n'

f'TIMES {report.Times}\n'

f'PROFIT {report.Profit}\n'

))

if __name__ == '__main__':

main()

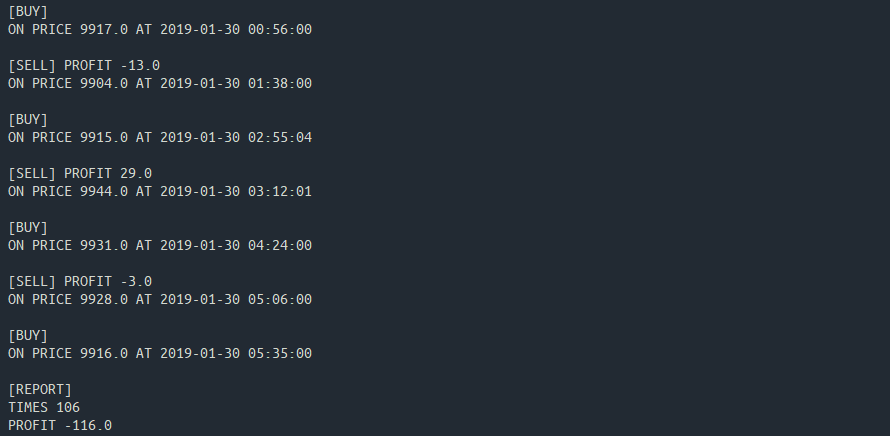

今年一月統計

交易:執行 106 次

相當於每個交易日執行 4-5 次交易

若這交易頻率不符心中預想規劃,那就要繼續修正策略

收益:虧損 116 點

恭喜!各位可以開始設計自己的策略,並使用這個簡單的回測系統進行初步的驗證囉!

投資有賺有賠,擁有工具的各位,還請慎重使用做好風控。

團隊系列文:

CSScoke - 金魚都能懂的這個網頁畫面怎麼切 - 金魚都能懂了你還怕學不會嗎

Clarence - LINE bot 好好玩 30 天玩轉 LINE API

Hina Hina - 陣列大亂鬥

King Tzeng - IoT沒那麼難!新手用JavaScript入門做自己的玩具

Vita Ora - 好 Js 不學嗎 !? JavaScript 入門中的入門。

TaTaMo - 用Python開發的網頁不能放到Github上?Lektor說可以!!