在產生日K、週K和月K資料之前,我們先將原本的SQLite資料庫,加上Index索引,以加快SQLite的存取速度。雖然建立Index會讓DB檔案大小變大,但卻可以讓資料庫的存取效率大大提升。

若要在SQLite中,建立Index可以透過兩種方式,第一個方式是用之前介紹的DB Browser for SQLite來建立Index

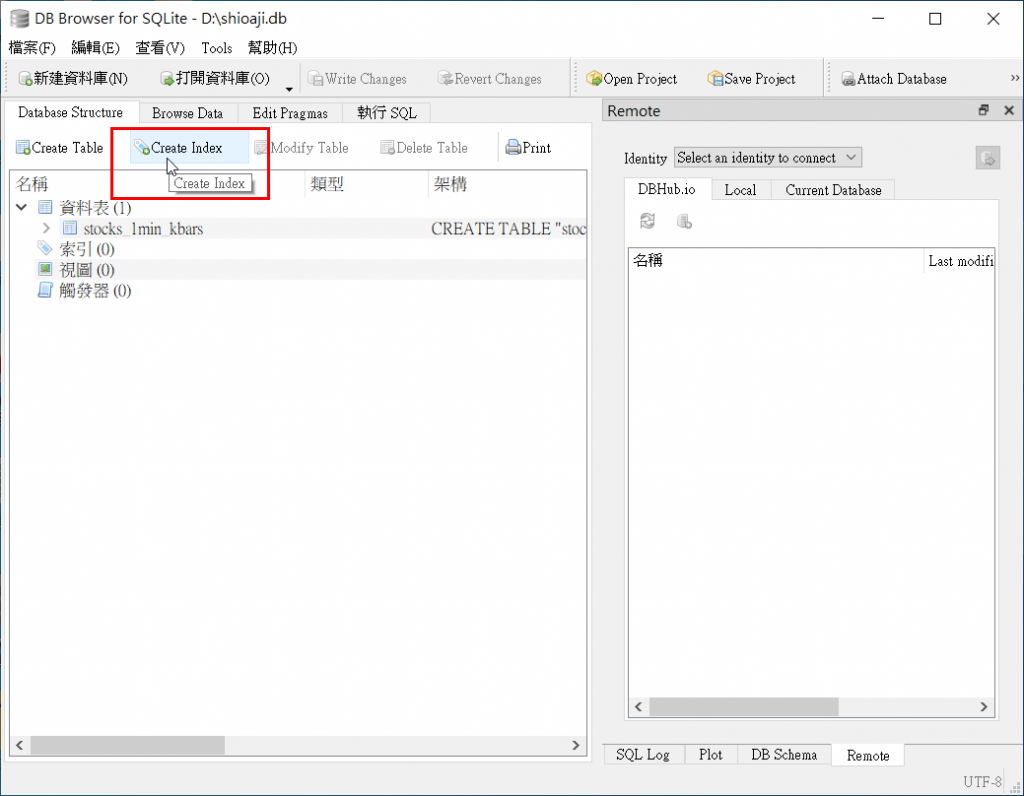

首先,執行DB Browser for SQLite並打開資料庫後,按「Create Index」

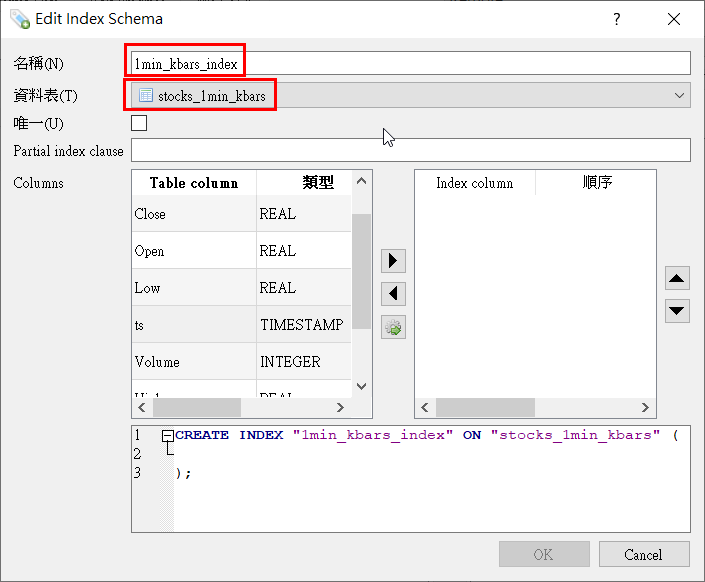

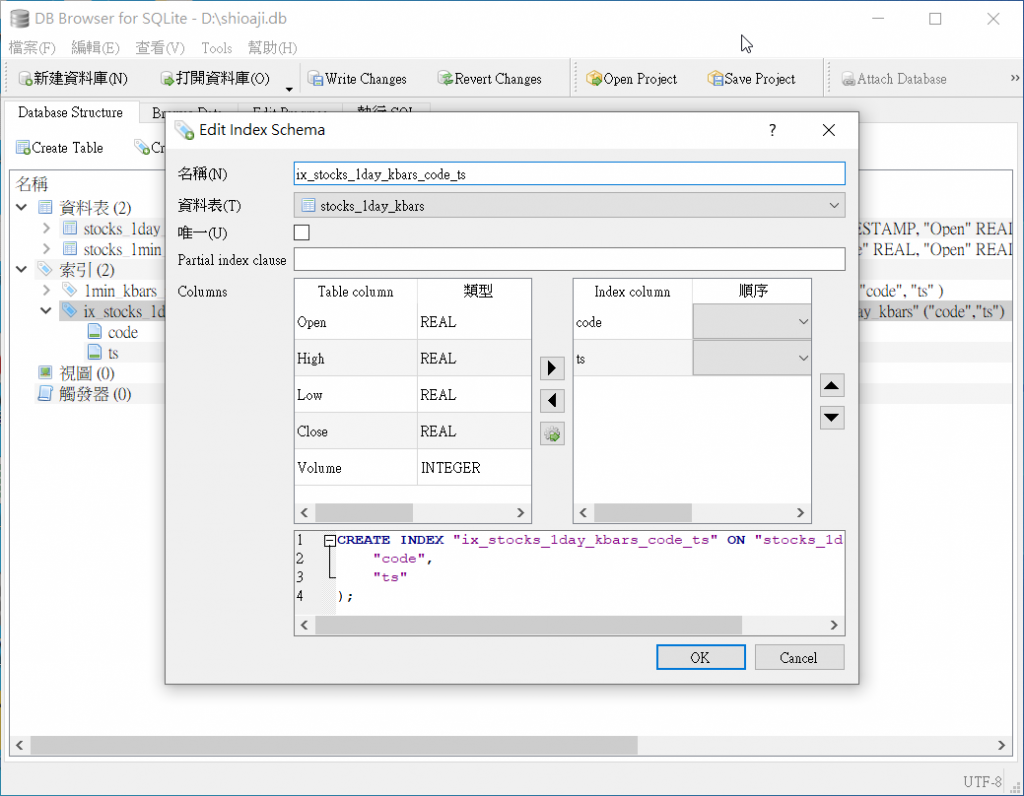

名稱請自行定義,而資料表則選擇你是要替哪個資料表建立索引,這裡我們選擇之前建立的1分K「stocks_1min_kbars」

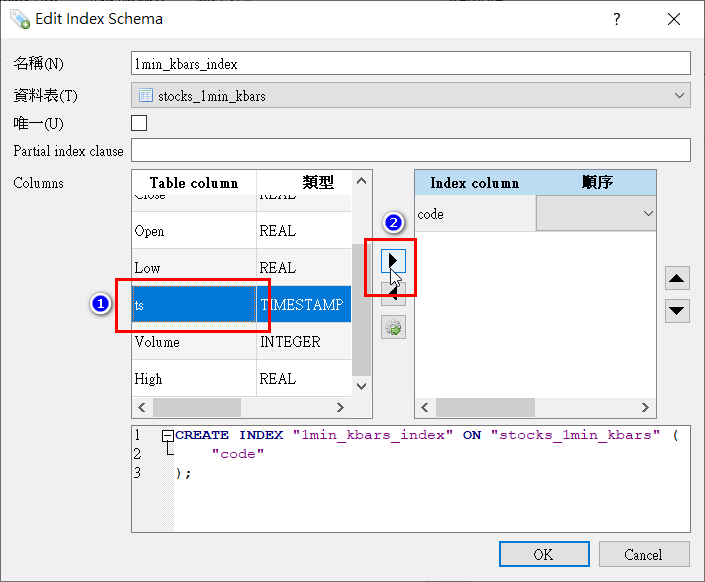

接著,選擇所要建立索引的欄位,選擇後請點「▶」按鈕將該欄位新增至右側的Index Column

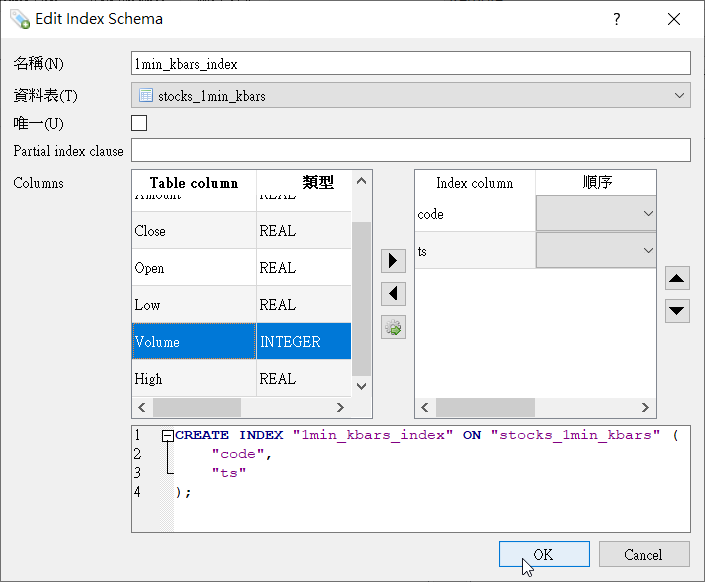

這裡我是選擇建立code及ts這兩個欄位的索引,確認後按下「OK」後,DB Browser for SQLite就會開始建立索引內容,此過程可能會因為資料量大而花上一點時間,請耐心等侯

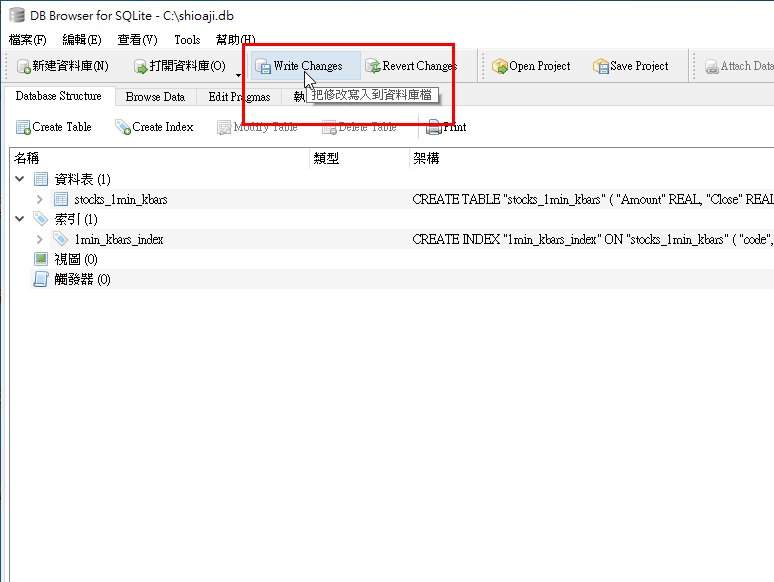

Index建立完成後,請按「Write Changes」,將剛才做的修改寫入資料庫中。

建立Index後shioaji.db檔案大小由7.35GB變為10.8GB,我跑了下列三檔股票的1分K轉5分K,並比較建立Index前後,執行pd.read_sql所需的時間(單位:秒)。可以看到讀取時間有大幅的減少。

| 股票 | 未建立Index,read_sql執行時間 | 建立Index後,read_sql執行時間 |

|---|---|---|

| 2330 | 94.51796960830688 | 0.5804615020751953 |

| 2890 | 15.362500667572021 | 0.5675475597381592 |

| 2890 | 15.250365018844604 | 0.5844612121582031 |

上面有提到,在SQLite可以手動建立Index來增加存取效率,除了上述的手動建立外,也可以透過pandas寫入資料時一併建立。我們以產生日K線資料為例,程式內容如下

import pandas as pd

import sqlite3

import time

conn = sqlite3.connect('D:/shioaji.db') #建立資料庫連線

# 傳入股票代碼,產生日K資料並存至資料庫

def generate_1day_kbar(stock_code):

print(f'generate 1dayK for stock:{stock_code}')

# index_col,產生DataFrame後將index設定為ts欄位

df = pd.read_sql(f'SELECT code, Open, High, Low, Close, Volume, ts FROM stocks_1min_kbars WHERE code = {stock_code}', conn, parse_dates=['ts'], index_col=['ts'])

# rule設為1D,表示resample為一天的資料

df_1day_kbar = df.resample(rule='1D').agg({

'code': 'first',

'Open': 'first',

'High': 'max',

'Low': 'min',

'Close': 'last',

'Volume': 'sum'})

df_1day_kbar.dropna(axis=0, inplace=True)

df_1day_kbar.reset_index(inplace=True) #重設index

df_1day_kbar.set_index(['code', 'ts'], inplace=True) #重新將Index指定為code、ts

df_1day_kbar.to_sql('stocks_1day_kbars', conn, if_exists='append')

print(f'stock:{stock_code}, 1dayK is added to DB...')

cursor = conn.cursor()

for code in cursor.execute('SELECT DISTINCT code FROM stocks_1min_kbars'):

generate_1day_kbar(code[0])

conn.close() #關閉資料庫連線

上面的程式中,我們在resample後先執行reset_index(),然後再次執行set_index,並將code及ts欄位傳入,這樣在執行to_sql時,pandas在建立資料庫table時,就會一併建立索引Index,執行DB Browser for SQLite並打開資料庫,就可以看到SQLite中已建立對應的Index。

若產生日K線資料,接著產生週K時,就可以直接抓stocks_1day_kbars中的資料去做處理。程式範例如下:

import pandas as pd

import sqlite3

conn = sqlite3.connect('D:/shioaji.db') #建立資料庫連線

# 傳入股票代碼,產生週K資料並存至資料庫

def generate_week_kbar(stock_code):

print(f'generate 1dayK for stock:{stock_code}')

df = pd.read_sql(f'SELECT code, Open, High, Low, Close, Volume, ts FROM stocks_1day_kbars WHERE code = {stock_code}', conn, parse_dates=['ts'], index_col='ts')

# resample並指定每週的最後一天為週五Friday

df_week_kbar = df.resample(rule='W-FRI').agg({

'code': 'first',

'Open': 'first',

'High': 'max',

'Low': 'min',

'Close': 'last',

'Volume': 'sum'})

df_week_kbar.dropna(axis=0, inplace=True)

df_week_kbar.reset_index(inplace=True)

df_week_kbar.set_index(['code', 'ts'], inplace=True)

df_week_kbar.to_sql('stocks_week_kbars', conn, if_exists='append')

print(f'stock:{stock_code}, weeK is added to DB...')

cursor = conn.cursor()

for code in cursor.execute('SELECT DISTINCT code FROM stocks_1min_kbars'):

generate_week_kbar(code[0])

conn.close() #關閉資料庫連線

產生月K線的資料,程式範例如下:

import pandas as pd

import sqlite3

conn = sqlite3.connect('D:/shioaji.db') #建立資料庫連線

# 傳入股票代碼,產生5分K資料並存至資料庫

def generate_month_kbar(stock_code):

print(f'generate month kbar for stock:{stock_code}')

df = pd.read_sql(f'SELECT code, Open, High, Low, Close, Volume, ts FROM stocks_1day_kbars WHERE code = {stock_code}', conn, parse_dates=['ts'], index_col='ts')

# rule指定為月

df_month_kbar = df.resample(rule='M').agg({

'code': 'first',

'Open': 'first',

'High': 'max',

'Low': 'min',

'Close': 'last',

'Volume': 'sum'})

df_month_kbar.reset_index(inplace=True)

df_month_kbar.set_index(['code', 'ts'], inplace=True)

df_month_kbar.to_sql('stocks_month_kbars', conn, if_exists='append')

print(f'stock:{stock_code}, month kbar is added to DB...')

cursor = conn.cursor()

for code in cursor.execute('SELECT DISTINCT code FROM stocks_1min_kbars'):

generate_month_kbar(code[0])

conn.close() #關閉資料庫連線