As I find out it's easier to type in Eng rather than switch the languages while I writing the articles.

Thus, I feel like to keep typing in Eng again ahaha, plz forgive me that I can't be bother to type in Mandarin lalala... ~ ~ ~

As stated earlier, ARIMA(p,d,q) are one of the most popular econometrics models used to predict time series data such as stock prices, demand forecasting, and even the spread of infectious diseases.

An ARIMA model is basically an ARMA model fitted on d-th order differenced time series such that the final differenced time series is stationary.

A stationary time series is one whose statistical properties such as mean, variance, autocorrelation, etc. are all constant over time.

ARIMA stands for AutoRegressive Integrated Moving Average

Auto Regressive Model forecast the values based on past values that have effect on current value. If we are about to forecast a monthly sales, then sales of November depends on sales of October, September and soon.

Time Series are stationary if the mean and variance is consistent over time. This happens only if they donot have trend or seasonal effects. A stationarized series is relatively easy to predict because of constant stationary terms

Moving Average model forecast the values based on previous days error terms that have effect on current value.

*Notice: You can print out the result by each step. Run the xxx.py for checkinig your code :)

*The dataset needs to have a column that contains date or time, as it needs a period of time's (Regression) dataset for the prediction. Good Luck! :)

Example dataset: Click ME !

Don't forget to do pip install pyramid-arima in Pycharm terminal, before you start the programing.

# coding: utf-8

import numpy as np

import pandas as pd

import sklearn

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

import matplotlib.pyplot as plt

import statsmodels.api as sm

from statsmodels.tsa.arima_model import ARIMA

Example dataset: Click ME !

df = pd.read_csv('usa_date.csv')

print(df)

## 決定訓練/測試數據要用的區間

## filter data after 2021-12

df = df['id']

df_train = df.iloc[328:449]

df_test = df.iloc[449:478]

#訓練數據整理

df_order= df_train.reset_index(drop=True)

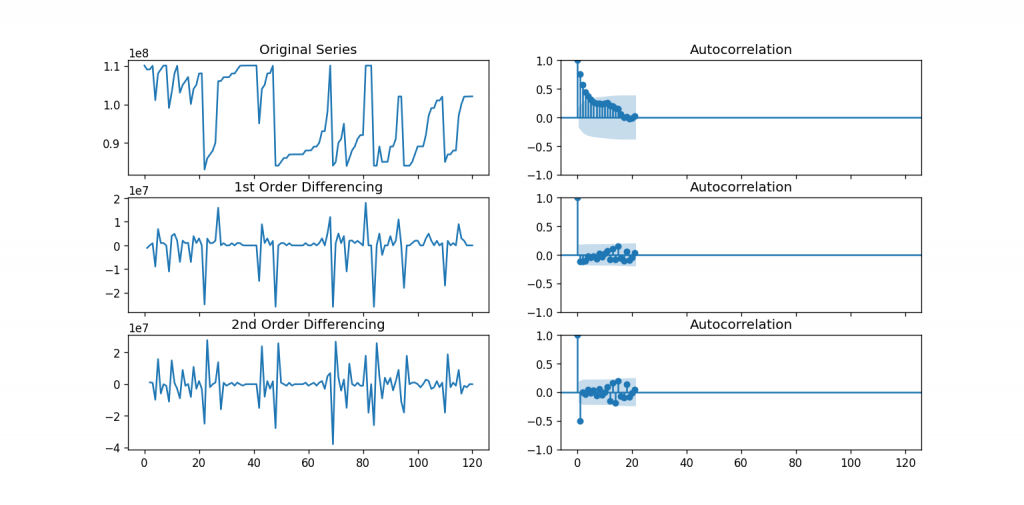

## acf plot

plt.rcParams.update({'figure.figsize':(9,7), 'figure.dpi':120})

# Import data : Internet Usage per Minute

df = df_order

# Original Series

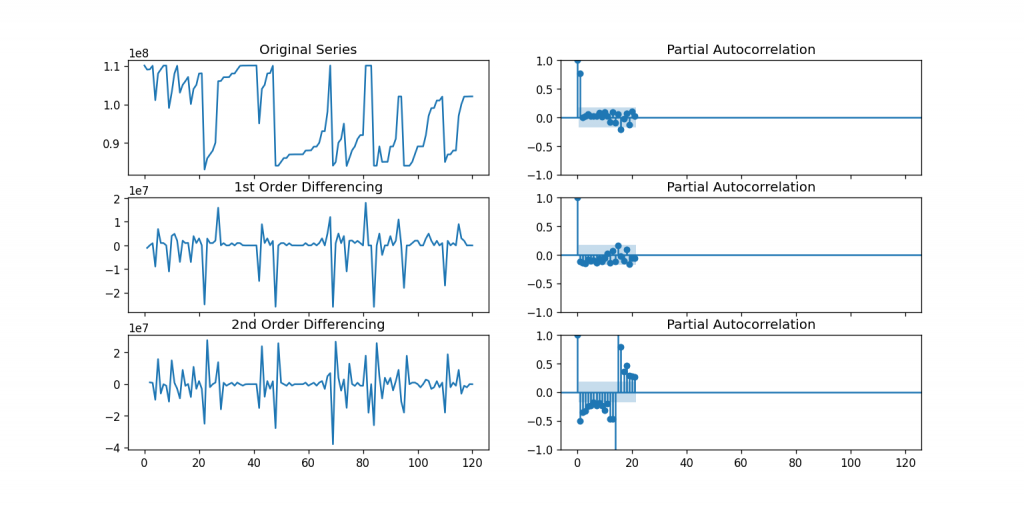

fig, axes = plt.subplots(3, 2, sharex=True)

axes[0, 0].plot(df_order); axes[0, 0].set_title('Original Series')

plot_acf(df_order, ax=axes[0, 1])

# 1st Differencing

axes[1, 0].plot(df_order.diff()); axes[1, 0].set_title('1st Order Differencing')

plot_acf(df_order.diff().dropna(), ax=axes[1, 1])

# 2nd Differencing

axes[2, 0].plot(df_order.diff().diff()); axes[2, 0].set_title('2nd Order Differencing')

plot_acf(df_order.diff().diff().dropna(), ax=axes[2, 1])

plt.show()

## pacf plot # Original Series

fig, axes = plt.subplots(3, 2, sharex=True)

axes[0, 0].plot(df_order); axes[0, 0].set_title('Original Series')

plot_pacf(df_order, ax=axes[0, 1])

# 1st Differencing

axes[1, 0].plot(df_order.diff()); axes[1, 0].set_title('1st Order Differencing')

plot_pacf(df_order.diff().dropna(), ax=axes[1, 1])

# 2nd Differencing

axes[2, 0].plot(df_order.diff().diff()); axes[2, 0].set_title('2nd Order Differencing')

plot_pacf(df_order.diff().diff().dropna(), ax=axes[2, 1])

plt.show()

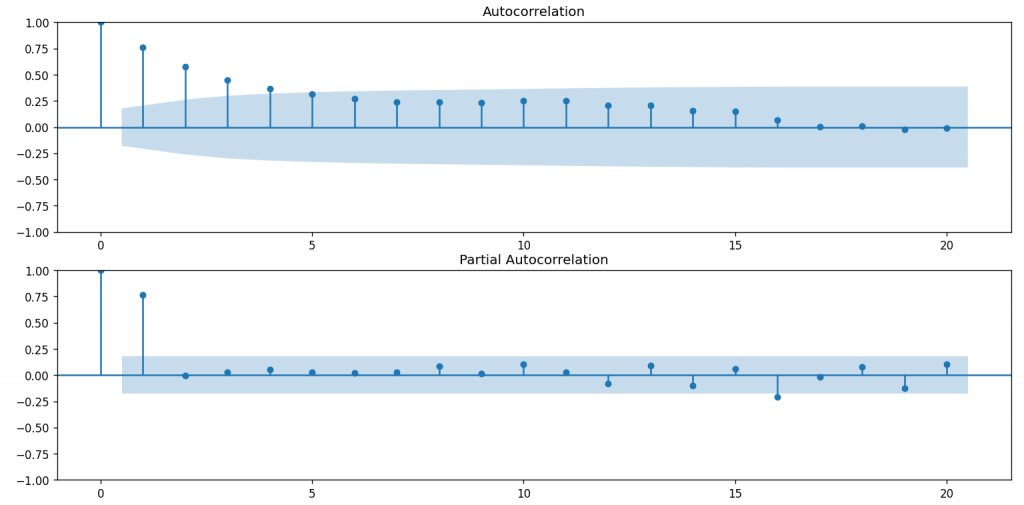

## 從acf 和pacf 圖『主觀地』決定我們arima 的d和p要設置多少

fig = plt.figure(figsize=(12,8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(df_order, lags=20,ax=ax1)

ax1.xaxis.set_ticks_position('bottom')

fig.tight_layout()

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(df_order, lags=20, ax=ax2)

ax2.xaxis.set_ticks_position('bottom')

fig.tight_layout()

plt.show()

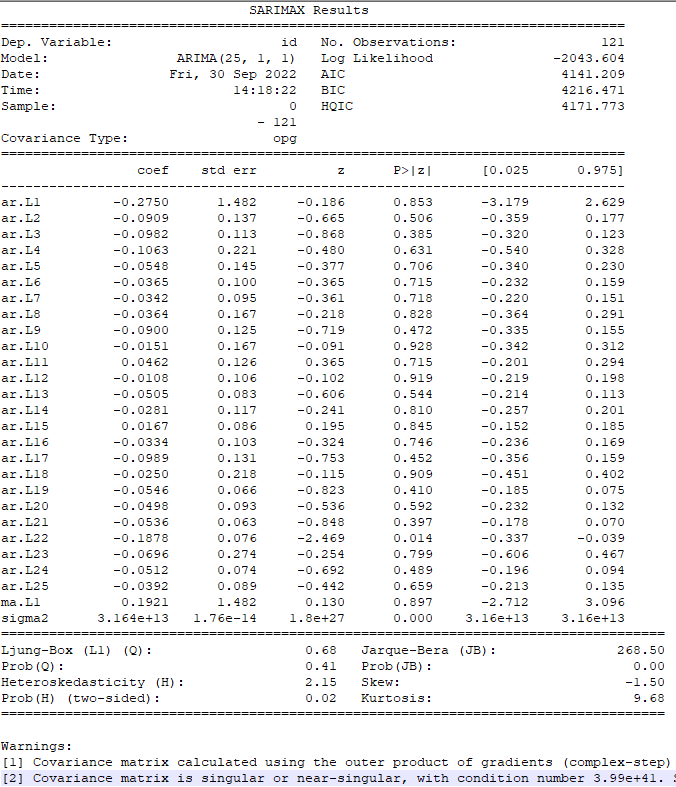

# 搭建ARIMA Model

model = sm.tsa.arima.ARIMA(df_order, order=(25,1,1))## p 設定和前n筆資料趨勢有關,d設定為1,q設定為1

model_fit = model.fit()

print(model_fit.summary())

## 重點關注指標,1.P值,2. coef

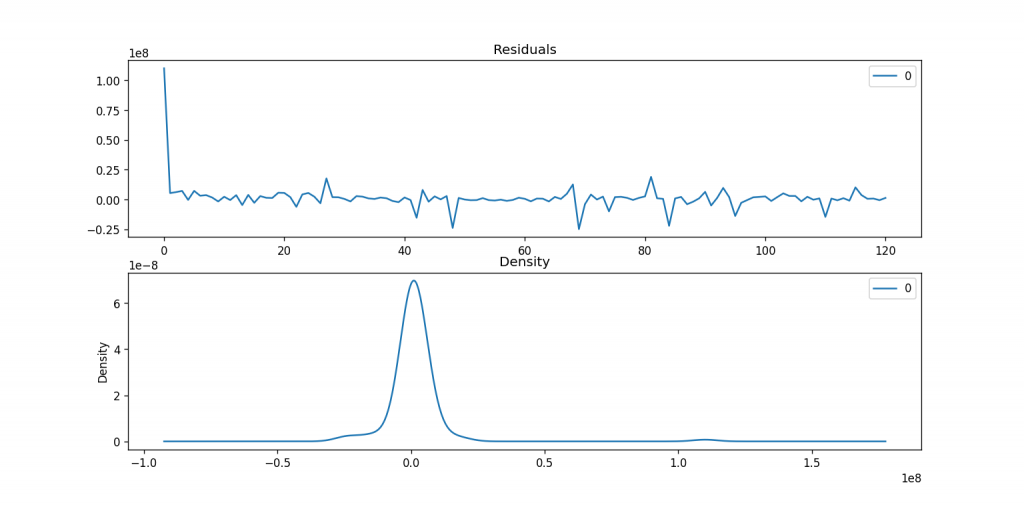

# Plot residual errors

residuals = pd.DataFrame(model_fit.resid)

fig, ax = plt.subplots(2,1)

residuals.plot(title="Residuals", ax=ax[0])

residuals.plot(kind='kde', title='Density', ax=ax[1])

plt.show()

### 輸出模型預測結果

prediction = model_fit.predict(1,150,dynamic=False)

print(prediction)

## 組裝訓練+期望預測數據

df_filter_test_2_2_1 = df_order.append(df_test,ignore_index=True)

print(df_filter_test_2_2_1)

## 視覺化

#visualize

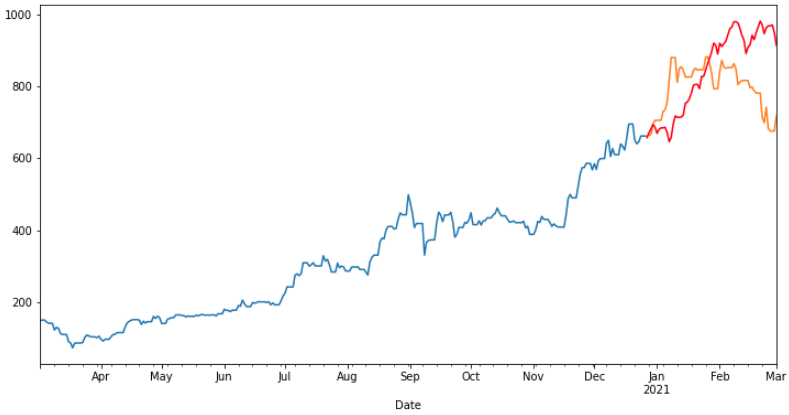

fig, ax = plt.subplots(figsize=(8, 5))

ax.plot(prediction,label = 'prediction',linestyle='--',color = 'red')

ax.plot(df_filter_test_2_2_1[120:150],label = 'real_order_202204', color = 'green')

ax.plot(df_order,label = 'real_history_data', color = 'gray',linestyle=':')

ax.set_xlabel('timestamp') # Add an x-label to the axes.

ax.set_ylabel('order count') # Add a y-label to the axes.

ax.set_title("order_predict") # Add a title to the axes.

ax.legend(); # Add a legend.

#!/usr/bin/python

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from statsmodels.tsa.arima_model import ARIMA

def date_parse(date):

return pd.datetime.strptime(date, '%Y-%m')

if __name__ == '__main__':

data = pd.read_csv('AirPassengers.csv', header = 0, parse_dates = ['Month'], date_parser = date_parse, index_col = ['Month'])

p,d,q = 2, 1, 2

data.rename(columns = {'#Passengers':'Passengers'}, inplace = True)

passengersNums = data['Passengers'].astype(np.float)

logNums = np.log(passengersNums)

subtractionNums = logNums - logNums.shift(periods = d)

rollMeanNums = logNums.rolling(window = q).mean()

logMRoll = logNums - rollMeanNums

plt.plot(logNums, 'g-', lw = 2, label = u'log of original')

plt.plot(subtractionNums, 'y-', lw = 2, label = u'subtractionNums')

plt.plot(logMRoll, 'r-', lw = 2, label = u'log of original - log of rollingMean')

plt.legend(loc = 'best')

plt.show()

arima = ARIMA(endog = logNums, order = (p,d,q))

proArima = arima.fit(disp = -1)

fittedArima = proArima.fittedvalues.cumsum() + logNums[0]

fittedNums = np.exp(fittedArima)

plt.plot(passengersNums, 'g-', lw = 2, label = u'orignal')

plt.plot(fittedNums, 'r-', lw = 2, label = u'fitted')

plt.legend(loc = 'best')

plt.show()

The other reference codes of ARIMA (full code) can refer to THIS LINK

iThome鐵人賽

iThome鐵人賽